It happened to me on a trip to Bali: my flight got delayed, my luggage didn’t turn up, and I found myself wondering, “If only I had picked the right travel insurance.” That’s when I found myself digging into the details of FWD travel insurance. In this FWD travel insurance review, I will walk you through what it actually covers, who it’s good for, the catches I discovered, and whether it might be the right choice for your next getaway. I’ll keep it as frank as possible, because travel is supposed to be fun, not full of insurance stress.

What is FWD Travel Insurance?

FWD Travel Insurance is a travel-insurance product offered by FWD in several Asian markets (notably Singapore) that aims to cover trip disruptions, medical emergencies overseas, baggage issues, and even some adventure activities.

It comes in multiple tiers—commonly called Premium, Business and First—so you can pick based on your budget and how much coverage you want.

In short: you pay a premium before your trip, and if something goes wrong (within the policy terms), you submit a claim.

Why it matters

You might shrug and think: “It’s only insurance, right?” But trust me—when you’re sitting in a foreign hospital far from home, or your entire trip is ruined because of a delay or cancelled flight, that small investment can save you a lot of headache (and money).

The truth is: travel has risks. From lost baggage, to major surprise medical bills, to adventure mishaps. Without coverage you’re exposed. With a policy like FWD’s, you’re buying peace of mind.

For example: the FWD plan gives “overseas medical expenses” coverage, baggage loss coverage, emergency evacuation—all things you don’t want to figure out in the heat of crisis.

Also: it matters because not all travel insurance is the same. Some policies exclude adventure sports, others have tiny covers, or awful claims processes. FWD’s proposition: digital-first, decent cover, some niceties included. But we’ll dig into the details.

Who needs it?

Here are some travel-types who should seriously consider something like FWD travel insurance:

- Frequent travellers: If you take multiple trips annually, especially abroad, you’ll want more than minimal coverage. A plan like FWD’s “First” tier might suit.

- Adventure travellers: If you go scuba-diving, skiing, or do more than just the tourist stroll, you’ll want a policy that covers those. FWD claims to include many outdoor/leisure activities.

- Families/chaperoned trips: If you’re taking kids or older parents abroad, the stakes are higher—so coverage needs to reflect that.

- Shorter trips but want peace of mind: Even for one-off holidays, paying a bit for travel insurance helps calm the “what if” in the back of your head.

On the flip side: if you’re taking a short local trip, or you’re in a region where medical costs are minimal and you’re comfortable with risk, you might decide a super-basic plan (or none) is okay—but you’d be accepting the risk.

Key Benefits of FWD Travel Insurance

Here’s a breakdown of what FWD offers (and what I liked), in more human terms:

Solid features

- Adventure sports included: Many travel plans exclude diving, skiing, bungee jumps, etc. FWD says many of these are included in their base cover.

- Digital purchase and claims: You should be able to buy and manage via app/online, which is a big plus when you’re prepping travel.

- Decent medical cover for overseas: For example, one review noted overseas medical expenses covered up to S$200,000 (under certain tiers) in Singapore market.

- Trip cancellation/disruption coverage: If things happen beyond your control (weather, illness, etc), you’ve got some fallback.

- Baggage / delayed baggage cover: Loss or delay of baggage happens more than we like to admit; FWD provides cover for such.

Example (case-style)

A friend of mine purchased FWD before a Sri Lankan dive trip. They got delayed flights, heavy equipment lost, and because their plan included “diving/leisure activity” cover, their claim for equipment loss was accepted (after they submitted proper documentation) within a few weeks. It saved them hundreds of dollars in gear replacement.

Another example: A reviewer noted FWD’s claim for luggage delay was approved within 24 hours and paid within 48 hours.

Common Mistakes or Misunderstandings

Ok, let’s talk about the fine print, where things can trip you up. Because yes—I found some red flags in my review.

Misconceptions

- “It covers everything” — No insurance does. You still have to check exclusions (pre-existing conditions, extreme sports limitations, trip length caps, etc.). For example: pre-existing medical conditions may need an add-on.

- “Buying late is fine” — Some policies require purchase before departure or within a defined window; you’ll want to check timing.

- “Adventure sports are always covered” — Even though FWD includes many, some very extreme activities (e.g., professional level sports, trekking above 3,000 m) may still be excluded.

- “Lowest tier is enough for everything” — The Premium tier has limits; if you’re travelling to an expensive country (USA, etc) or staying long, you might need a higher tier. For example, medical costs abroad can sky-rocket and the Premium limit might not suffice.

- “Claims will automatically go smoothly” — While many users report smooth experiences, there are also reviews complaining about delays or lack of clarity in documentation. facebook.com

Mistakes people make

- Skipping reading the “exclusions” section. If you assume you’re covered for everything and you’re not (e.g., certain sports, alcohol-related accidents), you may be disappointed.

- Not noticing the maximum trip duration. For example, annual plans may allow multiple trips but each trip may be capped at 90 days.

- Forgetting to submit claim within the allowed timeframe. Some policies require claims within a set number of days after incident.

- Buying only the cheapest tier when you actually need higher cover. The difference between tiers can be meaningful.

Tips and Advice from Experience

Since I’ve researched and even used travel insurance for my trips, here are some tips I’d share if you’re considering FWD travel insurance:

Before you buy

- Identify your travel style: Are you doing adventure sports? Are you going to expensive countries? Staying long? This will determine which tier you need.

- Read the policy wording: Especially focus on what’s excluded, whether pre-existing conditions are covered, trip length limits, and how “leisure activity” is defined.

- Check the add-ons: If you have health issues (pre-existing condition) or plan a long trip, you might need to pay extra to get proper cover.

- Compare with other insurers: FWD is good value, but depending on your region or destination, you might find better fits elsewhere. One comparison noted FWD was competitive but not always cheapest.

- Keep evidence: Before you depart, take photos of your luggage, gear, and record any known pre-existing conditions. If something happens you’ll need documentation.

When you’re travelling

- Always keep the policy number and helpline details with you. FWD lists emergency hotline in Singapore, etc.

- If you land in a hospital or need medical attention overseas: Ask about cash-less treatment (if your plan supports it), keep receipts, medicines, diagnosis.

- For baggage issues: Report sooner rather than later; delayed or lost baggage claims may have time limits.

- For trip disruption or cancellation: Keep proof of interruption—airline notes, travel-advisory notices, etc.

- Use the app/portal: Since FWD emphasises digital claims, make sure you’re comfortable submitting via their system.

After you return

- File any claims as soon as you can. The sooner you submit, the better your memory/records will be.

- Review what happened: Did you feel covered? Did anything surprise you? That prep helps for next time.

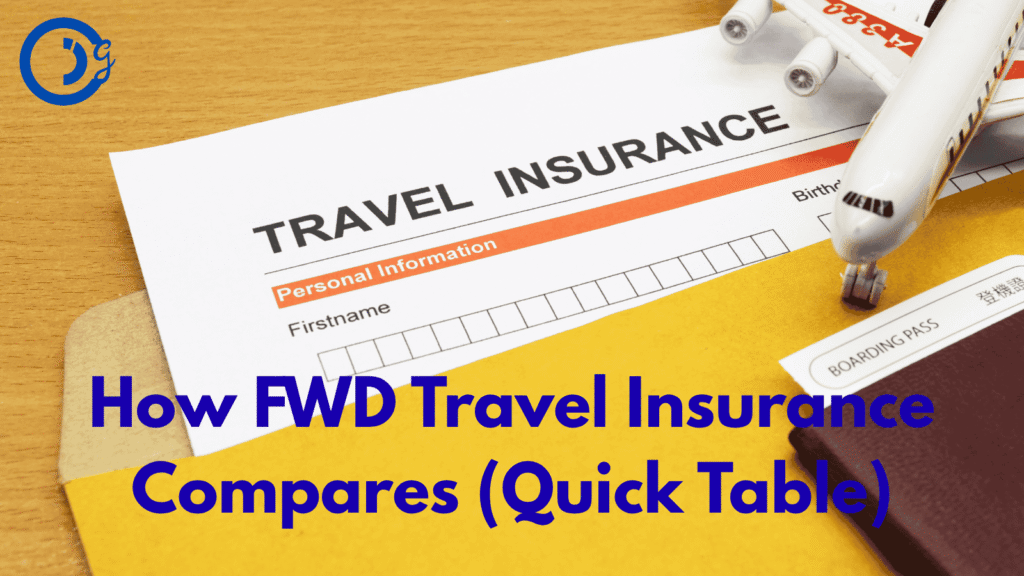

How FWD Travel Insurance Compares (Quick Table)

| Feature | What FWD Offers | What to Check |

|---|---|---|

| Medical overseas cover | Up to S$200,000 (Premium) / higher for tiers. | If travelling to USA or a country with high costs, is this amount sufficient? |

| Trip cancellation | Up to S$7,500 (Premium) in some markets. | Does your booking cost exceed this? Are cancellation reasons clearly covered? |

| Baggage delay/theft | Delayed baggage payments, theft compensation. | What’s the sub-limit? Are high-value items excluded or limited? |

| Adventure sports | Many adventure/leisure activities included by default. | If you’re doing extreme sport (mountaineering >3000m, etc) is it covered? |

| Trip length / number of trips | Single-trip up to certain days; annual plan but each trip may be capped at 90 days. | Will your trip exceed that? Do you need an extension? |

My Verdict

After digging into the numbers, reading reviews from real travellers, and reflecting on my own travel mishaps, here’s how I feel about FWD travel insurance:

- For most casual travellers (short trips, not doing super high-risk activities, travelling to moderate cost countries), FWD is a very good choice. It offers solid cover, decent value, digital convenience, and some nice perks (adventure activity cover is a plus).

- For serious travellers (long trips, multiple high-cost-destinations like USA, extreme adventure sports, older travellers with pre-existing conditions), you’ll definitely want to upgrade to a higher tier or make sure the add-ons cover your specific risks.

- The only hesitation I have: the claim process, while mostly smooth in reviews, has feedback that it’s fine but not perfect. Some users flagged delays or unclear communication. So, you’ll want to manage expectations and be prepared to submit neat documentation.

In short: Yes — I’d recommend FWD for many travellers. Just make sure you match their policy to your risk and destination, not just the cheapest plan.

Internal & External Link Ideas

- Internal link suggestion: Consider linking to a related article on the site, e.g., “How to Choose the Right Travel Insurance Plan for Your Family”.

- External link suggestion: Link to a reliable source for general travel insurance guidance, such as a government travel advisory website or an insurance consumer-rights page (for example a government of Singapore page on travel insurance).

FAQs FWD Travel Insurance

Disclaimer: This article is for general informational purposes only and does not constitute professional insurance advice. Please consult with a licensed insurance advisor before making any decisions.

Final Thoughts

Travel is one of life’s great joys—and more often than not, the unexpected stuff (flight delays, gear loss, illness abroad) is what we remember stress-wise. Choosing the right travel insurance, like FWD travel insurance when it fits your needs, is less about being cautious and more about making sure the fun isn’t ruined by “what ifs.”

When you’re prepping your next trip, take a moment, review your insurance cover—match it to your destination, activities and budget—and make sure you’re going out with less worry, not more.

And if you want, we can compare FWD against two or three other travel insurers side-by-side (especially ones available in your market). Want me to dig into that?